Q3 2018 Insights…

What’s FPC’s investment stance and how have the markets performed up to the end of September – find out more in our market commentary…

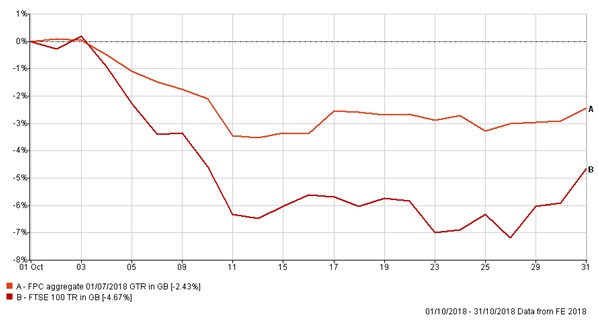

Last week our investment committee met to review our overall investment stance as well as how markets had performed to the end of September. Under normal circumstances a few weeks of data following the quarter end wouldn’t make a lot of difference. However, in the month of October, the FTSE 100 index of leading shares was at one point down by 7% before recovering slightly to end the month down 4.5%.

All FPC client portfolios are tailored to the needs of the individual investor and are individually reviewed but we do also monitor sample portfolios across the risk spectrum, so we can get an immediate view of what is happening under the bonnet and we’d like to share that insight with you.

An example of this is what we refer to as the ‘FPC aggregate portfolio’. This reflects our overall asset allocation policy and fund recommendations for a representative ‘medium risk’ portfolio.

In the month of October, the FPC aggregate fell in value by just 2.5% but that should be seen against the backdrop of previous returns of 28.5% over the last three years and 42.5% over the last five years.

It is over several years that the success of an investment strategy should be judged.

Individual clients will have experienced different fluctuations, some more and some less. This depends mostly on the portfolio’s asset allocation – portfolios with a greater percentage invested in shares are likely to have fallen further than portfolios adopting a more ‘defensive’ approach. Please note past performance is not a guide to future performance.

What is FPC’s current stance?

A typical ‘medium risk’ portfolio comprises around 45% in ‘fixed interest’ investments such as corporate bonds and around 55% in ‘growth assets’ such as property and shares (equities).

Within the equity element we have exposure to developed markets across North America, Europe and Asia, as well as a specific allocation to emerging markets.

Over the years, our investment committee has gradually introduced more global exposure to portfolios and this has resulted in better returns with lower volatility than a predominantly UK-focused or ‘home-biased’ portfolio.

What has unsettled the markets recently?

Looking to October really doesn’t tell us anything substantive but there have been a number of issues which are collectively influencing markets in the short term.

Economic activity was sluggish at the start of the year with the ‘Beast from the East’ and continued uncertainty due to Brexit (which still prevails). Meanwhile economic activity in the EU slowed because of weakening demand and threats of Transatlantic trade wars.

In the last quarter, growth in the EU has increased and is ahead of some estimates and the EU Central Bank has announced an end to Quantitative Easing by the New Year and is unlikely to raise interest rates until late next year.

In contrast, in the US, the Federal Reserve raised interest rates for the third time this year reflecting a labour market at near full employment, building wage pressure and inflationary fears.

Taken together these factors are having an impact on confidence.

So, what should you do?

The answer is ‘Nothing’. We actively encourage clients not to get distracted by short-term market movements. In all cases portfolios are positioned to reflect individual risk tolerances and objectives. They are broadly diversified and designed to withstand the unexpected.

We have always also maintained that every investor should hold a healthy cash reserve so that no asset is ever sold at a depressed price. And that an investor’s goals and risk profile should be regularly reassessed to ensure that their portfolio matches their current needs.

This is part of our regular review process for all clients, but please contact us if you would like to discuss your unique circumstances in more detail.