By Stephen Caffrey – Chartered Financial Planner at FPC

Your business is likely to be your most significant asset and main source of income so your financial planning needs to take the future of the business into account.

When you sell your business, it is essential to not just focus on maximising the final sale price. You should also consider what effect that sum of money will have on you and your family’s estate.

Capital Gains Tax & Business Asset Disposal Relief

Under current rules, on sale, the business owner is liable to capital gains tax on the sale proceeds. Providing the owner meets specific criteria, they can claim Business Asset Disposal Relief (BADR), previously known as Entrepreneurs Relief, meaning you have the opportunity to claim up to £1 million pounds at the rate of 10%. The rest will be taxed at the current rate of 20%.

Here’s the core qualifying criteria you’ll need to meet:

- You must be an employee of officer of the company (including being a company director, secretary etc.) or a sole trader.

- You must own at least 5% of the company share capital, including voting rights and be entitled to at least 5% of profits or the disposal proceeds.

- You must have held the shares for a minimum of 2 years.

- The business must be a trading company. However, If the company stops being a trading company, you can still qualify for relief if you sell your shares within 3 years.

*Extra £100k tax saving opportunity: If you have a spouse, there is an opportunity to transfer some of your shares to your partner providing the two-year rule and other conditions are met. This can mean you qualify for two Business Asset Disposal Reliefs (two lots of £1 million at 10%) as transfers between spouses and civil partners can take place on a no loss, no gains basis.

Inheritance Tax & Intergenerational Wealth Planning

As well as capital gains tax, you also need to consider inheritance tax and intergenerational wealth planning.

Currently, a trading business that has been running for over two years can qualify for business relief, meaning the value of your business is either partially or fully protected from the current inheritance tax rate of 40%. However, once the business sale goes through and you are in cash, you lose that relief and fully expose yourself to the 40% rate.

Of course, there are opportunities to pass on your wealth throughout your lifetime, but they often come with various complications and costs.

You can make outright gifts to family members and friends. However, outright gifts over the annual allowances need seven years before they fully transfer out of the donor’s estate for Inheritance tax purposes. Additionally, direct gifts give no protection to the money or the beneficiary if they are financially immature, vulnerable or run into relationship issues.

Trusts

Another way of giving money away during your lifetime, and post-sale, is establishing a trust. Again, this has the same seven-year clock issue, but there is protection for the asset and the beneficiary, as your trustees (which can include yourself) can decide on when they receive the money and for what reason.

However, one of the main issues with trusts is the limit on how much can be transferred in without an immediate tax implication. This limit is currently £325,000 per person. Anything above this will be subject to an immediate, and generally unattractive, inheritance tax charge of 20%.

Trusts & The Pre-Sale Opportunity

A unique opportunity exists to potentially pass more than £325,000 without attracting the 20% tax rate. You do this by gifting a percentage of your shareholding into a trust before the sale. As the shares qualify for business relief, they are inheritance tax exempt on the way in.

It is essential to note that the transfer of shares into the trust will be deemed a disposal for capital gains tax purposes. However, gift holdover relief is available, meaning the tax can be deferred to a later date.

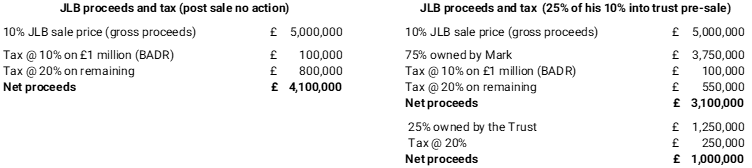

Example case: Mark (age 55, single, unmarried) owns 10% of JLB limited and is approaching selling his share of the business for £5 million. He has a son, Jeremy, age 21, who is moving out to go to university and has proven untrustworthy with money recently.

Capital gains tax on sale (no action vs transferring shares into trust pre-sale)

As you can see, Marks’s exposure to capital gains tax remains the same. However, Mark mustn’t give too much away as he could jeopardise his own business asset disposal relief if his stake drops below 5% or the £1m value threshold.

Inheritance tax on sale (no action vs transferring shares into trust pre-sale)

As you can see, as long as Mark has lived past seven years since the gift of shares into trust, he will have managed to move £1 million out of his estate, which equates to a potential saving of £400,000. It is worth noting that this is only a family saving as Mark will have sadly passed for this saving to be realised.

Trusts are not just about shielding wealth from Inheritance tax. Trusts are valuable tools to help protect and control assets. In this example, the trust can help Jeremy and future generations financially, whether funding university costs, providing a regular income, or even buying Jeremy a home to live in. All this can be done whilst the trust and trustees maintain control and protect the family’s financial wealth.

But be aware: Trusts do require a level of administration and ongoing reporting to HMRC and they’re also subject to periodic charges to inheritance every ten years so they are not without complications and specialist advice should be sought before taking any action.

Summary

Putting shares into a trust before a business sale can reduce your longer-term inheritance tax exposure with the added benefit of protecting the assets for your family. However, it’s vital not to put too much money into trust as you need to be confident you no longer need to access the funds for your personal use. This can especially be difficult if you are young and want to retire on the sale proceeds. Not only do you need to calculate your cash requirements year on year, but you also need to factor in unforeseen events, inflation and the possibility of long-term care. We can help you make those assessments as that is what financial planning is all about!

As business owners, FPC understands the lifetime commitment and personal sacrifices you have made to build your business and how important it is to protect that legacy and those who rely on it for financial security. Speaking with a financial planner, reviewing the finer details and completing cash flow modelling can help you plan for this event. To find out how we’ve helped other business owners to plan their journey and control their future, give us a call on 01704 571777 or email me on stephen@fpc.co.uk.