In July this year the Chancellor charged the Office of Tax Simplification to review capital gains tax. They have now reported back with a 136-page report (with another to follow) which as anticipated, proposes bringing income tax and capital gains tax rates in line with each other and a removal of the capital gains tax free exemption that currently applies on death.

In July this year the Chancellor charged the Office of Tax Simplification to review capital gains tax. They have now reported back with a 136-page report (with another to follow) which as anticipated, proposes bringing income tax and capital gains tax rates in line with each other and a removal of the capital gains tax free exemption that currently applies on death.

In this article, Paul Welsh, Chartered Financial Planner at FPC considers the implications for investors.

The current rules

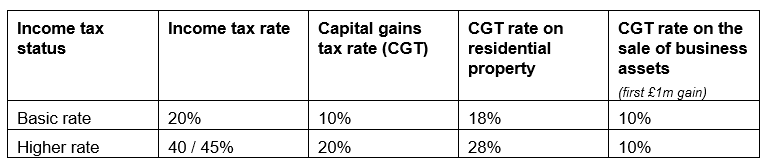

Capital gains tax was first introduced in 1965 and has swung back and forth depending on who has been in charge at No 11 Downing Street. The current tax rate differentials between income tax and capital gains tax are as follows:

It has long been argued that this discrepancy is acceptable as it acts as incentive that rewards risk taking and promotes enterprise but the relatively small number of beneficiaries of this system has been highlighted as leading to those individuals paying proportionally less tax than others. As a result, we have expected change for some time and have factored that into our planning for clients.

Allowances could be slashed

However, somewhat unexpectedly and at odds with the concept of alignment of tax rates, the report suggests a significant reduction in the annual capital gains tax allowance which stands at £12,300 per person per tax year currently, to as little as £2,000 to £5,000 per annum, yet the current income tax free annual allowance would presumably still stand at £12,500.

The report does raise some concerns about what impact this may have on investor behaviour and whether it might create an incentive for taxpayers to hold assets through companies, as Corporation Tax is (currently) charged at a lower rate.

Business owners retained profits in the spotlight

There is also a suggestion that any review of capital gains tax needs to be integrated with a review of inheritance tax which has again been a matter of debate for some time and particular attention is given to the taxation of accumulated earnings within owner managed businesses with the suggestion that retained profits might be taxed as dividends and not given capital gains tax treatment in the event of a sale or wind up of a business. This would undoubtedly have an impact on the approach taken to remuneration by business owners and would affect exit planning and investment decisions.

The key message here is that change is undoubtedly coming even though these reforms might only raise c. £14bn in tax which is dwarfed by the £200bn hole in the country’s finances so further tax rises may also follow.

Paul comments: “We have always taken a position that tax diversification is as important as investment diversification and we incorporate a range of tax wrappers such as ISA’s, investment bonds, pensions and general investment accounts into client portfolios to give flexibility to adapt income delivery strategies as things change. That stance is reinforced by today’s report.

We are also advocates of ‘tax harvesting’ and each year, as part of our annual review with clients, we will review how best to utilise annual capital gains tax allowances, rebasing gains as we go so as not to waste allowances that might otherwise be lost.

With the deficit in the government’s finances widening due to the support provided to businesses during the pandemic and the lack of appetite for further austerity, we have been anticipating these changes for some time and have been factoring them into our planning reviews for all clients where relevant.

This is when the value of financial planning can be clearly differentiated from financial advice and we would encourage all investors to review their circumstances now and in the run up to the end of the tax year. Our whole team stand ready to help and welcome referrals as appropriate to those who are concerned and need guidance.”

You can access the full OTS report at this link and we will provide further analysis and comment once the second report is published. As always, if you have any queries or concerns, don’t hesitate to contact us.