The team at FPC is privileged to have been asked to present a series of talks on financial literacy for law graduates at BPP University Law School, although they would be equally relevant for any young professionals.

The team at FPC is privileged to have been asked to present a series of talks on financial literacy for law graduates at BPP University Law School, although they would be equally relevant for any young professionals.

In the first of the talks, FPC Senior Adviser, Paul Welsh talks about the basic principles of investment and looks at some of the behavioural influences that impact on our decision making…

When we hear the word ‘investment’ certain images may come to mind. That could be the traditional trading floors of Wall Street or the London Stock Exchange, or the rather outrageous behaviour of the likes of Jordan Belfort (the real-life Wolf of Wall Street, author and convicted felon who swindled millions of dollars out of investors in the 1990s).

Throughout recent history, there have been loads of stories of easy investment returns and tales of fortunes to be made overnight. In recent times, the more extreme messages tend to be that we can make enough money to retire, or that we can make a living from trading for just a few hours a day.

Ultimately, these stories tap into some of our base emotions. It tends to feel exciting to talk about investments and large returns. However, there is a saying in the investment world, ‘win by not losing’ and if we follow a few basic principles, we can avoid the pitfalls.

1. The seven basic principles for successful investing:

Separate savings from investment

Before you even consider investing money, it is important that we separate savings from investment. Obviously, you should budget and live within your means but it is good practice to retain an appropriate cash reserve for emergencies. For young professionals, this could be 6 months’ worth of your basic expenses, plus you should keep aside money for any known, one-off expenditure within the next 5 years.

Don’t invest money that is needed in the short term. It is return of capital, not return on capital that is the most important consideration here. Short term investment does not allow enough time to ride out market downturns.

Understand and manage risk

Generally speaking, the higher the return, the more risk you need to take in order to achieve that return. And at a certain point along that risk scale ,a higher degree of risk doesn’t translate into the same increase in return.

There are no risk-free investment returns to be found but there are plenty of opportunities to take return-free risks. As the saying goes, if something seems too good to be true, it probably is.

Diversify your portfolio

Diversify your portfolio

One of the main ways we can manage risk is through diversification (this is the only free lunch in investment).

By spreading your investments across a range of different asset classes, with exposure to a wide range of global stock and bond markets, you are spreading the risk you are taking.

Avoid market timing

Jordan Belfort was quoted on the BBC in February as saying that trying to decide when to sell shares in a company is basically like trying to catch a falling knife on the way down. You are probably going to get hurt.

So, don’t try to call the top or bottom of the market. It is time in the market, rather than market timing, that will have the biggest impact on investment returns.

Fear inflation

Inflation has been in the news recently, as the global economy emerges from the pandemic and the disruption it caused feeds through to consumer prices.

Inflation is a serious threat to wealth. If it is running at 3% in 10 years’ time, £10,000 will be worth just £7,400 in real terms, losing over a quarter of its value.

Inflation is a reason to invest over the long term to try to preserve the purchasing power of your money in future years.

Manage tax and costs

Costs can have a significant impact on investment returns. Some investment fund costs, for example, can be pretty eye-watering. The annual charges on typical investment funds can range from 0.1% per year to as high as 3.5%. Add in inflation to the latter and you are giving yourself a high hurdle rate from the outset.

Chartered Financial Planner, Helen Thomas covers tax planning in a bit more detail in Talk 2 but avoiding unnecessary tax and using all of the legitimate allowances and reliefs available will also increase overall returns. It is the net of tax and costs return which matters!

So, focus on managing these so you keep as much of the return as possible.

Stay disciplined

Finally, simply having a plan and sticking to it gives you the best chance of yielding favourable results.

And talk of discipline leads into something that I have touched upon already and is often overlooked, but which has started to receive more and more attention in investment circles in recent years – the impact our emotions have on the decisions we make.

2. Behavioural influences

2. Behavioural influences

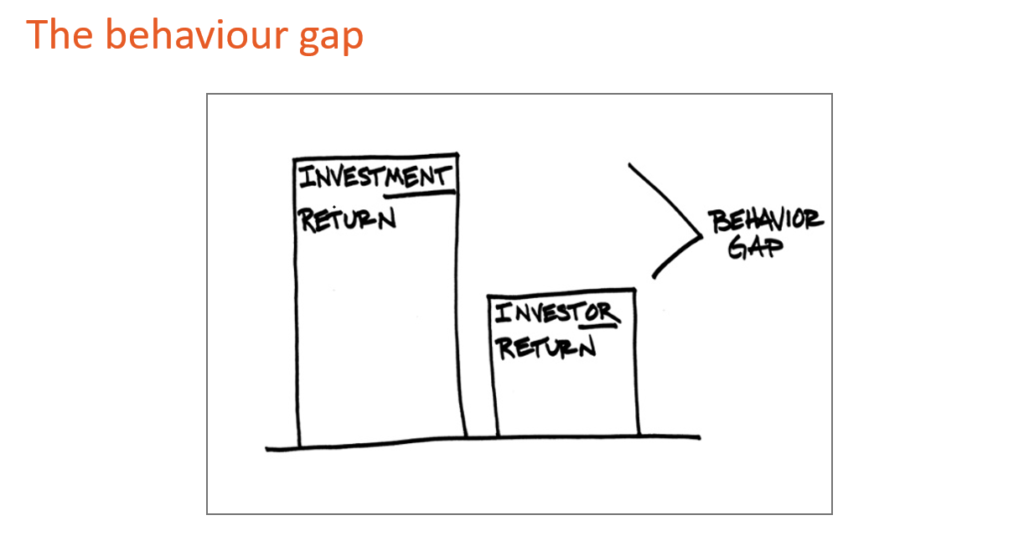

We like to imagine that we make rational decisions, but generally we tend to react emotionally. Despite what we think, we are more Homer Simpson than Spock!

Studies have shown that the returns an investment portfolio generates naturally are higher than the returns investors typically realise because their own behaviour tends to have a sub-optimal impact on their investment portfolio.

These behaviours are innate and arise from the primitive part of our brain and so we are all susceptible, even educated professionals, but following the principles I have just outlined will help us to mitigate those behaviours.

Ultimately, investment boils down to managing the risks to your wealth:

- the risk of running out of or losing money

- the risk of the purchasing power of your money being eroded over time

- the risk of not achieving what you want to achieve.

Warren Buffett is regarded as one of the greatest investors of all time, yet his overall philosophy is very simple. When he invests, he does so for the long term and doesn’t attempt to time markets. He diversifies by buying shares in various different companies and he holds them for a long period of time.

3. In Summary

- focus on the things you can control

- build a cash reserve

- invest for the long term

- spread your risk

Good investing is not about making great decisions. It’s about consistently not making mistakes or in other words, we win by not losing!

Check out our blogs for the other talks:

Talk 2: Helen Thomas on Tax Planning and Pensions

Talk 3: Will Carter on Insurance Products

Talk 4: Stephen Caffrey on Understanding Debt

Or visit our YouTube channel to watch all four talks: https://youtu.be/AKXu-mSO4t4