The team at FPC is privileged to have been asked to present a series of talks on financial literacy for law graduates at BPP University Law School, although they would be equally relevant for any young professionals.

The team at FPC is privileged to have been asked to present a series of talks on financial literacy for law graduates at BPP University Law School, although they would be equally relevant for any young professionals.

In our final talk, Chartered Financial Planner at FPC, Stephen Caffrey talks about debt, types of interest, credit scores and student loans…

Introduction

Debt is something that all of us will encounter during our lives. It’s important to point out that not all debt is bad. For example, mortgages are considered to be a good form of debt as they can provide young people with independence (and an opportunity to escape from the parents!).

Bad forms of debt tend to be short term with high interest rates, such as overdrafts and pay day loans.

The office of national statistics findings shows that around 40% of people aged 22-29 have no savings at all, whilst 10% have around £2,000 to £3,000 and only 25% have over £6,000. Therefore, all it takes is losing a job or a broken-down car for you to get started in the debt spiral.

Although young professional people are expected to be more financially mature, it’s important that they fully understand how to avoid some of the pitfalls associated with debt.

What is debt?

- Debt is money borrowed from one party to another such as loans, mortgages and credit cards.

- When you borrow money you will pay back the original amount (called the capital) plus the interest (which provides the lender with compensation for bearing risk).

- Interest is usually defined as APR (annual percentage rate) which tells you the cost of borrowing.

- Secured vs Unsecured: Secured debt is collateral backed (eg. if you fail to make mortgage payments, the provider can repossess your home) and usually offers a better interest rate whereas unsecured is not collateral backed (eg. credit cards with interest rate determined primarily on credit score).

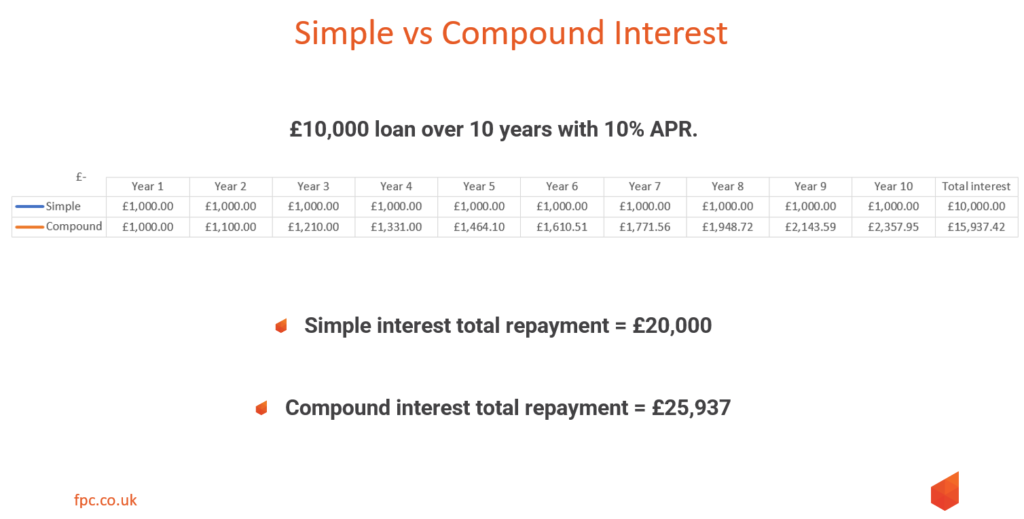

Simple vs Compound Interest

Focusing on the interest element, there are the two most popular forms of interest, which are simple and compound. Simple interest is a fixed percentage of the original sum borrowed year on year, and compound interest is interest added to interest.

Here you will see the difference between simple vs compound on £10,000 loan over 10 years, with a 10% interest rate

As you can see you will pay more interest using the compound method. Compound is used by most lenders including credit card and payday lenders.

Credit cards are currently around 30% APR whilst some payday loan lenders have a rate of 766% APR, so, when compared with the 10% shown in the graph it shows you just how easy a debt can get out of hand if the interest is left to accumulate and compound.

Factors determining the level of interest charged

Here are the three main ones:

Secured vs unsecured (mentioned earlier) – when collateral is involved you usually benefit from a better interest rate.

Credit score – a person’s credit score is shown as a numerical value representing an individual’s credit worthiness. The better your score the more likely you are to obtain a higher amount of credit at a lower interest rate. So, if you pay your debt on time and don’t miss any payments, the more likely you are to have a better credit score.

Strangely, people who have debt but make the payments on time can have a better credit score than people who have absolutely no debt. This is because it proves the individual has a track record of keeping promises and paying back their debt on time, whereas the lender has no information on the person with no debt, so the risk is higher.

You can check your credit scores by signing up with companies like Experian. Companies like these can also help review your score, suggest changes to improve your score and make sure there are no errors or inconsistencies in your report.

Credit scores may not be considered to be a priority for most young professionals but it’s advisable to monitor and improve your credit score to ensure you are able to obtain the best terms for loans.

The Bank of England – the rate that it charges banks and lenders to borrow money (The Bank of England influences what rate of interest banks and lenders charge consumers for mortgages, loans and other credit).

Student Loans

Student loans are often sold as a cheap form of borrowing that most students won’t even notice coming out of their wages when they start work.

A debt trap you can easily fall into is paying back some of your student loan debt by making regular or one-off voluntary contributions. Paying back debt earlier is usually a good thing but in the case of student loans it’s not always the case, due to the uniqueness of the debt being wiped after 30 years.

Here’s a couple of examples of two different approaches:

- Student A and student B leave university in the same year on the same terms with the same debt (£55,000), and both enjoy a 5% annual salary increase.

- Student A earns a starting salary of £40,000, whilst student B earns a starting salary of £25,000.

- Student A pays back £133,000 and has £24,000 worth of debt wiped at year 30.

- Student B pays back £44,000 and has £152,000 worth of debt wiped at year 30.

Are voluntary contributions worth it?

- Both student A and B decide to make an additional voluntary contribution of £100 a month or £1,200 a year.

- Student A pays back his debt after 25 years and saves £22,500.

- Student B still doesn’t pay back the debt, but it has cost them and extra £36,000.

Using extra money to pay of student loans is not a priority for most young people as they will probably have other priorities, such as buying their first home, going on holiday, buying a car and having kids.

So, to conclude, student debt is not as cheap as they say and making voluntary contributions may not be worthwhile unless you are a top earner, have ticked off most of your life goals and have paid off your debts. Always check the math’s before making any decisions.

In Summary:

- Beware compound interest – it’s easier than your think to get yourself in a debt spiral so try not to overexpose yourself, especially to short term “bad” debt were possible.

- Do your maths – before making any decision on entering into a new credit agreement, shop around to get the best interest rates and if you are thinking about making voluntary contributions to your student loan, complete a calculation (Sites like money saving expert have online calculators to help you).

- Take debt seriously – even missing a few payments on a mobile contract or gym membership can be the difference between getting the mortgage amount for your dream home or obtaining a loan with a workable interest rate to fund a business idea.

Check out our blogs for the other talks:

Talk 1: Paul Welsh on Savings & Investment

Talk 2: Helen Thomas on Tax Planning, Pensions & Saving for the Future

Talk 3: Will Carter on Insurance Products

Or visit our YouTube channel to watch all four talks: https://youtu.be/AKXu-mSO4t4