The team at FPC is privileged to have been asked to present a series of talks on financial literacy for law graduates at BPP University Law School, although they would be equally relevant for any young professionals.

The team at FPC is privileged to have been asked to present a series of talks on financial literacy for law graduates at BPP University Law School, although they would be equally relevant for any young professionals.

In the second of the talks, Chartered Financial Planner at FPC, Helen Thomas talks about the basic principles of tax planning and pensions and provides a few pointers on what to look out for…

Tax Planning

- Tax code – always check that payroll and HMRC have your correct tax code, especially if you’re starting a new job as emergency codes are sometimes used which can result in overpayments or underpayments.

- Tax allowances – make sure you take advantage of all the tax allowances available ie. Personal Allowance, pension annual allowance, ISA allowance, capital gains tax allowance etc. as you may be paying more tax than you should, which will have an impact on any investment returns.

- Tax laws & legislation – legislation affects the allowances that you may be entitled to so make sure you take advantage of them while they last.

Pensions

Saving for retirement probably isn’t a priority for most young professionals but there are some simple things that you can do that your future selves will thank you for:

- Say yes to being auto-enrolled and don’t be tempted to want to keep all your income in your pocket – don’t forget your employer will be making a contribution to your pension too so for example, if you earn £30,000 and are required to put £1,500 in a pension, your employer will contribute £900 or sometimes more!

- Make additional pension contributions via your employer’s scheme if you can – you won’t pay as much income tax or national insurance as your gross income (income before tax) will be less and some employers will give you the additional national insurance that they save for your pension.

- You can also make additional pension contributions via a separate pension scheme

Pension contributions are ultimately a good and ‘legal’ way of reducing your income tax bill whilst saving for the future.

ISAs

- Make sure you don’t invest in a non-tax efficient wrapper (generally called General Investment Accounts) as your ISA allowance is currently £20,000 so make sure you use it (and this could change following new legislation).

- Make sure you understand how ISAs work and the different types, ie. cash ISAs and shares ISAs – the £20,000 allowance can be split between the two and one can be transferred to another.

- Don’t invest all your money into an ISA without thinking about how much you’ll need to live on – you may be forced to sell in a depressed market meaning that you get back less than you put in.

Other Investments

- Don’t be tempted to join tax avoidance schemes to reduce your tax bill – remember what happened to Jimmy Carr.

- There are legitimate schemes but they come with risk, eg. VCTs, EIS and SEIS – they usually need a substantial investment and invest in high-risk businesses.

- Remember if it sounds too good to be true, it generally is – you may get 10, 20, 100% returns but with a lot of luck and risk!

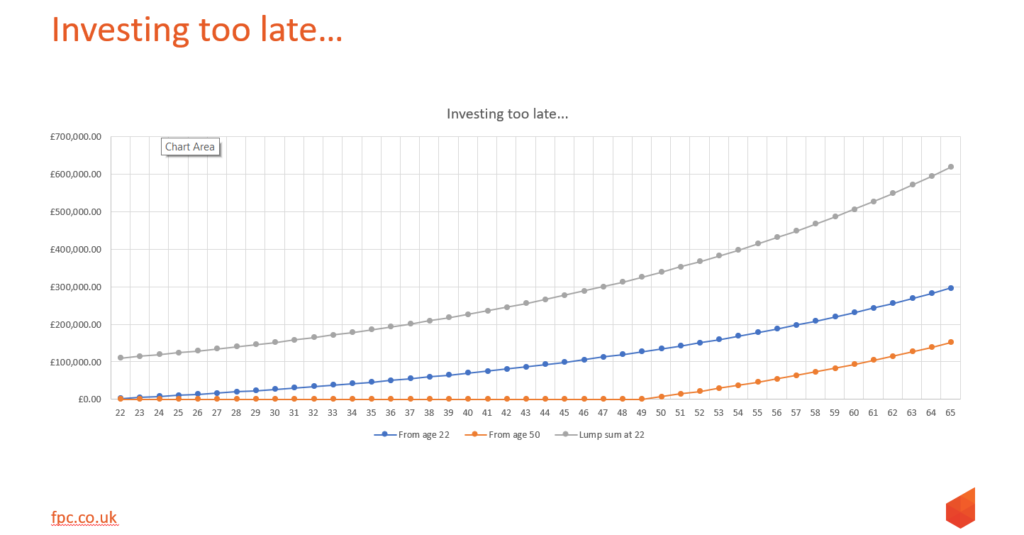

Investing now vs in the future

We’ve talked a lot about investing now instead of waiting until your close to retirement but why does everyone recommend this? Well, this chart helps illustrate why:

- Blue shows your investment if you put in £200 per month from age 22 to 65 – in total, you pay £105,600 into your pension.

- Orange shows your investment if you don’t start investing until age 50 but you still make a total of £105,600 into your pension. It’s invested for 15 years as opposed to the 44 years if you started at 22 – the difference is £145,000 by 65!

- The grey line really does show the impact of time in the market – the whole of £105,600 is invested at 22 and nothing is added to this – you get almost £620,000 back after 44 years!

This chart assumes a growth rate of 4% per annum after charges and is obviously stagnant but really does illustrate the power of saving early vs waiting until it’s almost too late.

In Summary – So what can you do for yourselves today then?

- check your tax codes and make sure HMRC know who you are

- make sure you are aware of tax allowances and make use of them where possible

- don’t say no to auto-enrolment

- don’t leave pension planning until your old!

Check out our blogs for the other talks:

Talk 1: Paul Welsh on Savings & Investment

Talk 3: Will Carter on Insurance Products

Talk 4: Stephen Caffrey on Understanding Debt

Or visit our YouTube channel to watch all four talks: https://youtu.be/AKXu-mSO4t4